Español

Español

English

English

UFI, the Global Association of the Exhibition Industry, has released the latest edition of its flagship Global Barometer research, which takes the pulse of the industry.

Results highlight the severe impact of the COVID-19 pandemic on the exhibition industry worldwide, in 2020. There are also positive signs regarding a quick recovery in 2021

Globally, between April and August 2020, more than half of all companies reported no activity. This situation changed from September, where the majority of companies declared some operations, at reduced levels for most. Looking ahead to 2021, the share of companies expecting a return to “normal” activity is expected to grow from 10% in January to 37% in June.

These results vary depending on region, and are primarily driven by the “re-opening date” of exhibitions. In all regions, most companies expect both local and national exhibitions to re-open by the end of June 2021, with international exhibitions resuming in the second half of the year. Company operations also include, while face-to-face events are not possible, working into the development of digital solutions

When asked what element would most help with the “bounce back” of exhibitions, the majority of companies, ranked “readiness of exhibiting companies and visitors to participate again” (64%), “lift of current travel restrictions” (63%) and “lift of current public policies that apply locally to exhibitions” (52%) as key factors.

Overall:

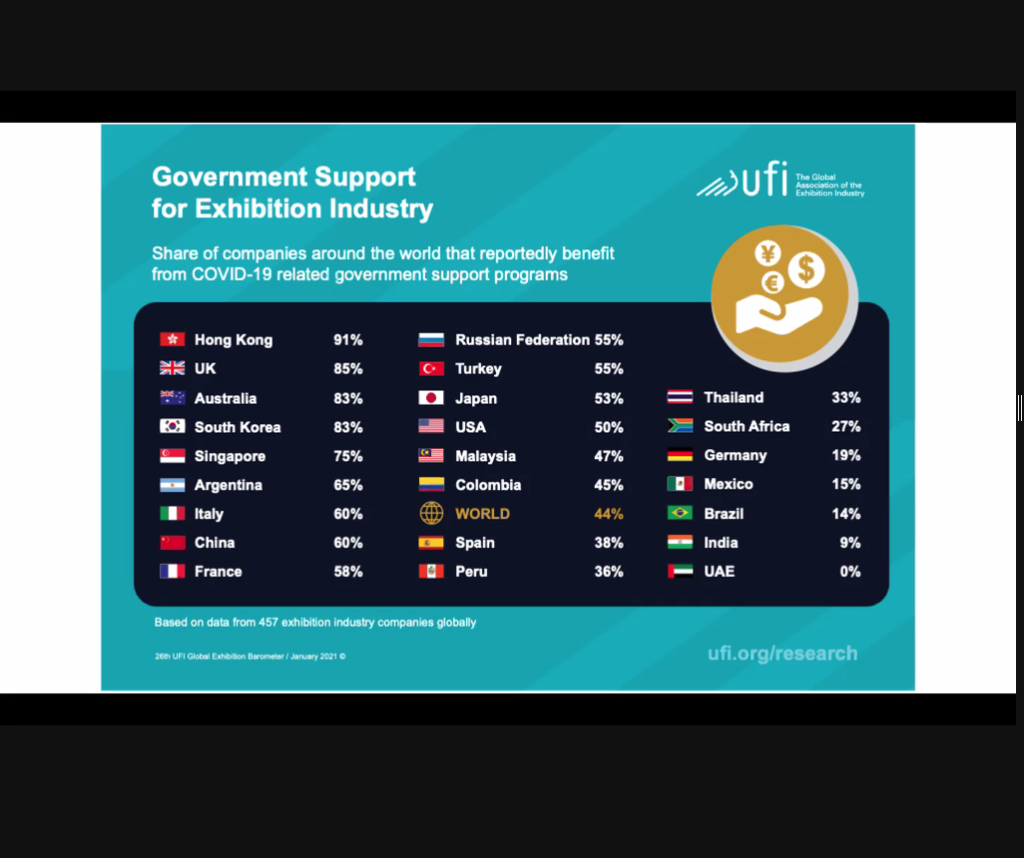

- 44% of companies benefitted from some level of public financial support; for the majority this related to less than 10% of their overall 2019 costs.

- 54% of companies had to reduce their workforce, with half of these by more than 25%.

- 10% of companies will have to consider permanently ceasing operations if there are no events for the next six months.

As expected, the “impact of the COVID-19 pandemic on the business” is considered the most important business issue (stated by 29% of companies, a 2% increase on six months ago). The “impact of digitalisation” (11%) and “competition with other media” (7%) have also increased (+1% and +2% respectively), while the “state of the economy in the home market” (19%) and “global economic developments” (16%) have decreased, but remain amongst the top three concerns.

In terms of future exhibition formats, global results indicate that 64% (compared to 57% six months ago) are confident that “COVID-19 confirms the value of face-to-face events”, indicating an expectation that the sector will bounce back quickly.

“The message from the global industry is clear: quite simply, 2020 was horrible. The pandemic stopped most activities around the world for several months, and, globally, our industry’s revenue dropped by almost three quarters. But, as the Global Barometer shows, 2021 should see a significant bounce back, with global revenues expected to double, pending markets re-opening and clarity on regulations. We will ‘build back’ even better, and while the industry will remain, primarily, a face-to-face marketing channel, digital offers will evolve with new patterns,” says Kai Hattendorf, UFI Managing Director and CEO.

Size and scope

This latest edition of UFI’s bi-annual industry survey was concluded in December 2020, and includes data from 457 companies in 64 countries and regions.

The study also includes outlooks and analysis for 24 countries and regions – Argentina, Australia, Brazil, China, Colombia, France, Germany, Hong Kong, India, Italy, Japan, Malaysia, Mexico, Peru, Russia, Singapore, South Africa, South Korea, Spain, Thailand, Turkey, the UAE, the UK and the US – as well as an additional five aggregated regional zones.

“We sincerely thank all companies who took part in this study. The results from 29 markets and regions provide strong insights for assessing both the impact of the crisis and future perspectives. We also welcome AFEP and UNIMEV, who partnered with us for this edition, resulting in our first ever specific country profiles for Peru and France,” says Christian Druart, UFI Research Manager.

Operations since 2020 – reopening exhibitions:

Results show that the periods when most companies reported “no activity” in 2020 were limited to March-June for the Asia-Pacific region, April-June for North America, and April-September for Central and South America and the Middle East and Africa. In Europe, there was an initial period of inactivity in April-August, followed by another period in November-December.

Turnover – operating profits

Regional Results indicate that:

The revenue drop for 2020 was the highest for companies in Central and South America and the Middle East and Africa (who respectively only achieved 23% and 24% of 2019 revenue levels). Companies in the Asia-Pacific region (27% of 2019 levels), Europe (32% of 2019 levels) and North America (36% of 2019 levels) are at or above global averages. The 2021 perspectives are rather similar for all regions: who are expecting to achieve between 32% and 37% of last year’s revenue for H12021, and between 55% and 60% for all of 2021.

In terms of profits, the share of companies who faced a loss for 2020 varies from 47% in the AsiaPacific region and Europe, to 50% in North America, 58% in the Middle East and Africa, and 64% in Central and South America.

Public financial support – workforce and perspectives

Regional results indicate that:

The number of companies receiving public financial support is higher in Europe (54% of companies) and the Asia-Pacific region (53%), than in Central and South America (35%), North America (31%) and the Middle East and Africa (13%).

The share of companies forced to reduce their workforce is higher in the Middle East and Africa (73% of companies), North America (61%) and Central and South America (56%), than in Europe (52%) and the Asia-Pacific region (49%).

The proportion of companies believing they will need to close if business doesn’t resume within the next six months varies from 5% in North America, to 6% in the Asia-Pacific region, 10% in Central and South America, 14% in Europe and 17% in the Middle East and Africa, while the proportion of companies who believe they will cope ranges from 26% in Europe to 40% in the Asia-Pacific region.

Key business issues

While the “impact of the COVID-19 pandemic on the business” is the key business issue across all regions, “global economic developments” are ranked higher in the Middle East and Africa (23% of companies) than in other regions. The “impact of digitisation” is ranked higher in North America (15%) and Europe (14%) than other regions.

Further insight by type of activity, for three main segments – organisers, venues and service providers – highlights a difference in the fourth most important issue, with organisers indicating “impact of digitisation”, venues indicating “internal challenges” and service providers indicating “regulatory/stakeholders’ issues”.

Future exhibition formats

The report also highlights two significant regional differences in relation to possible trends driving the future format of exhibitions:

- The claim “COVID-19 confirms the value of face-to-face events” was more widely agreed with in the Middle East and Africa (70% of companies), the Asia-Pacific region (69%) and Europe (67%), than in North America (55%) and Central and South America (53%).

- While, there were stronger opposing views for the claim “virtual events replacing physical events”, with 74% of companies in Europe disagreeing, compared to just 57% of companies from North America.

Background

The 26th Global Barometer survey, conducted in December 2020, provides insights from 457 companies in 64 countries and regions. It was conducted in collaboration with 20 UFI Member Associations: AAXO (The Association of African Exhibition Organisers) and EXSA (Exhibition and Event Association of Southern Africa) in South Africa, AEO (Association of Event Organisers) in the UK, AFE (Spanish Trade Fairs Association) in Spain, AFEP (Asociación de Ferias del Perú) in Peru, AFIDA (Asociación Internacional de Ferias de América) representing Central and South America, AKEI (Association of Korean Exhibition Industry) in South Korea, AMPROFEC (Asociación Mexicana de Profesionales en Ferias, Exposiciones, Congresos y Convenciones) in Mexico, EEAA (Exhibition & Event Association of Australasia) in Australia, IECA (Indonesia Exhibition Companies Association) in Indonesia, IEIA (Indian Exhibition Industry Association) in India, JEXA (Japan Exhibition Association) in Japan, MACEOS (Malaysian Association of Convention and Exhibition Organisers and Suppliers), in Malaysia, MFTA (Macau Fair & Trade Association) in Macau, RUEF (Russian Union of Exhibitions and Fairs) in Russia, SECB (Singapore Exhibition & Convention Bureau) in Singapore, SISO (Society of Independent Show Organizers) in the US, TEA (Thai Exhibition Association) in Thailand, UBRAFE (União Brasileira dos Promotores Feiras) in Brazil and UNIMEV (French Meeting Industry Council) in France.

In line with UFI’s objective to provide vital data and best practices to the entire exhibition industry, the full results can be downloaded at www.ufi.org/research

The next UFI Global Barometer survey will be conducted in June 2021.

About UFI – The Global Association of the Exhibition Industry:

UFI is the global trade association of the world’s tradeshow organisers and exhibition centre operators, as well as the major national and international exhibition associations, and selected partners of the exhibition industry. UFI’s main goal is to represent, promote and support the business interests of its members and the exhibition industry. UFI directly represents more than 50,000 exhibition industry employees globally, and also works closely with its 60 national and regional association members. More than 800 member organisations in 83 countries around the world are presently signed up as members. Around 1,000 international trade fairs proudly bear the UFI approved label, a quality guarantee for visitors and exhibitors alike. UFI members continue to provide the international business community with a unique marketing media aimed at developing outstanding face-to-face business opportunities.

Press Release from UFI.

Comments 0